Education loans can be a lifeline for students aspiring to study in premier institutions, but over time, repayment conditions or interest rates may become overwhelming. That’s where education loan transfers come into play. This process allows borrowers to shift their existing loan to another lender, often securing more favourable terms, such as lower interest rates, better repayment schedules, or enhanced customer service. This guide explores everything you need to know about education loan transfers in 2025, from eligibility criteria and benefits to the step-by-step transfer process. With expert tips to help you maximise savings, this blog aims to empower you to make informed financial decisions and get the most out of your education loan transfer.

Let’s First Understand What An Education Loan Transfer Is

Here’s how an education loan transfer from one bank to another works. Let’s say that you have taken an overseas education loan from NBFC because of their shorter processing period and a year later, you are not happy with their student loan repayment scheme and would like to apply for a student loan refinancing from a public bank. In such a scenario, you may apply for a Education loan transfer from your NBFC to a banking institution.

Types Of Education Loan Balance Transfer

When it comes to managing education loans, many borrowers look for ways to reduce their financial burden. One such option is an education loan balance transfer, which allows students to shift their existing loan from one lender to another. This process is typically pursued to secure better interest rates, more favourable repayment terms, or tax benefits. Whether you are moving from a secured loan to an unsecured one or switching between unsecured loans, understanding the types of transfers available can help you make informed financial decisions and potentially save money on your loan. Let’s explore the different types of education loan balance transfers and how they can benefit you.

| Type of Loan Transfer | Description | Key Benefit |

| Secured to Secured | Transfer from one secured loan to another secured loan, where both loans are backed by collateral. The process is completed with Xerox copies of collateral documents. | Keeps the loan secured without needing new collateral. |

| Unsecured to Secured | Transfer an unsecured loan (from private banks/NBFCs) to a secured loan (from government banks). Borrowers can secure their loan with collateral and get a lower interest rate. | Reduces interest rates by offering collateral. |

| Unsecured to Unsecured | Transfer an unsecured loan from one private lender to another. Often chosen to benefit from tax advantages like Section 80E, which reduces tax liability on interest payments. | Tax benefits on interest payments (Section 80E). |

| Secured to Unsecured | Rare transfer from a secured loan (lower interest rate) to an unsecured loan (higher interest rate). This usually happens when the collateral is sold to pay off the loan. | Frees up the collateral, but increases interest rates. |

How To Transfer Federal Student Loan To Another Lender Or Servicer?

Education loan transfer to other banks involves a specific process. Here are the general steps you can follow:

Step 1: Contact Your Current Servicer

Action: Reach out to your current loan servicer to discuss your desire to transfer your loans.

Purpose: Inquire about any options available for transferring or refinancing your loans and understand the process.

Step 2: Research and Choose a New Servicer or Lender

Action: Compare different federal loan servicers or private lenders if considering refinancing.

Purpose: Look for better customer service, repayment options, or lower interest rates. If refinancing, ensure you meet the eligibility criteria of the new lender.

Step 3: Complete the Transfer or Refinancing Process

Action: If refinancing with a private lender, submit your application and required documentation. Once approved, the new lender will pay off your existing loan.

Purpose: Confirm that your old loan is closed and begin making payments to your new servicer or lender according to the new terms.

Eligibility Criteria For The Transfer Of Educational Loan

When considering transferring an educational loan from one lender to another, borrowers typically need to meet specific eligibility criteria. Here are the key requirements based on the search results.

| Criteria | Details |

| Current Loan Status | Completion of Disbursements: The borrower must have received all scheduled disbursements from the current lender. No further disbursements should be pending. |

| Repayment Track Record | Good Repayment History: Borrowers should have a consistent repayment history with their existing lender, as it helps maintain a good credit score. |

| Minimum Loan Amount | Some lenders may require a minimum loan balance for transfer eligibility (e.g., a minimum of ₹10 lakh in India). |

| Collateral Requirements | For transferring from an unsecured loan to a secured loan, appropriate collateral documentation must be provided as per the new lender’s requirements. |

| New Lender’s Criteria | Borrowers must fulfil the eligibility criteria set by the new lender, such as academic progress, financial stability, and co-applicant income verification. |

| Documentation | Complete all necessary documentation required by the new lender, including loan applications, identity proofs, income proofs, and statements from the current lender. |

| Co-Applicant Requirements | A co-applicant (such as a parent or guardian) may be required to provide proof of income and other relevant documents, depending on the lender’s policies. |

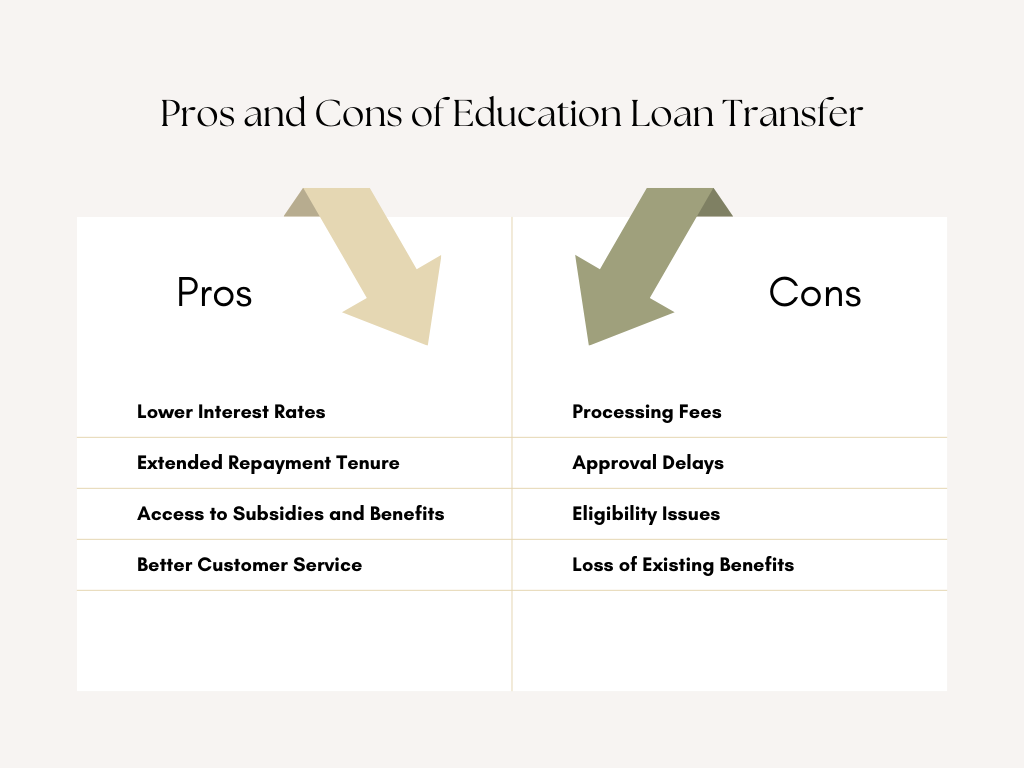

Pros And Cons Of Education Loan Transfer

An education loan transfer can be a useful financial tool for students looking to reduce their interest rates or secure better repayment terms. However, like any financial decision, it comes with both advantages and disadvantages. Understanding the pros and cons of an education loan transfer can help you make the best decision for your financial situation.

What Should You Be Aware Of During The Transfer Process?

When transferring a federal student loan to another lender or servicer, it’s crucial to be aware of several factors to ensure a smooth process and avoid potential issues. Here are key considerations:

Check out your final financial outflow: By offering lower EMIs, at a low student loan interest rate and a longer maturity schedule, modern banks aim to draw buyers, which may seem appealing on the face of it, but it may turn out to be more costly in the final analysis. So, determine how much you would potentially pay in both scenarios, and then consider which situation will be more appropriate for you. Experts will advise you to stick with your current bank and pay greater EMIs if you are not too hard-pressed for cash, finish off your loan sooner, even if the interest rate for education loans is higher, and rest easy.

It is important to calculate processing and other fees beforehand: Think how much you are paying out, and what the new bank will charge for a transaction tax, stamp tax, appraisal cost, and legal costs, then balance it against the interest rate cut. If you find that the new education loan in India is still cheaper after taking these items into consideration, then you should go with it, or else stick to the old education loan.

Associated account requirements: If you take out an education loan in India, banks normally require you to open a savings account with them so that they can route your EMIs via it. So, if you intend to transfer student loans to another bank, this aspect would also need to be taken into consideration closing one savings account and opening another with another bank, and the costs it will require.

Relations matter: Personal relationships do matter in banking, as in all other sectors; they will make the operation and procedures simpler. In other words, the simplicity of doing business leads to a great deal of peace of mind. If you transfer student loans to another bank and the workers don’t comply much, it will only raise your problems, mess with your professional job, and make life more complicated in general. So, in those cases, Education loan transfer may not be worth it.

Collateral ratio to outstanding ratio: If you have already repaid a substantial part of your loan, don’t give your current bank absolute original collateral. Why would you agree to offer a security that is double the value of your loan outstanding? Instead, you can use it to take an extra loan, if the need emerges. Give a smaller sum of collateral to the current bank. And if the bank also persists on the same matter, bargain more to lower the interest rate.

Final Steps When Loan Transfer Is Being Serviced

The final steps when your loan transfer is being serviced involve ensuring a seamless transition and updating your records accordingly. Here’s a guide to the concluding steps:

| Step | Description |

| Confirmation of Transfer | Confirm with both current and new loan servicers that the transfer is complete, ensuring loan balance and terms are accurate. |

| Update Contact Information | Ensure your updated mailing address, email, and phone number are provided to the new loan servicer for notifications. |

| Set Up Online Account | Set up an online account with the new servicer to easily manage payments, track your loan, and view your repayment progress. |

| Review Repayment Schedule | Review the new repayment schedule, confirming due dates, amounts, and any changes to your repayment plan. |

| Update Automatic Payments | If you use automatic payments, update the payment details with your bank to avoid disruptions. |

| Monitor Loan Status | Regularly check the loan status with the new servicer to ensure payments are applied correctly and resolve any discrepancies. |

| Stay Informed about Benefits | Confirm that any federal benefits (e.g., loan forgiveness or income-driven repayment) remain in place after the transfer. |

| Save Documentation | Retain all documents, including confirmation notices and communication with both loan servicers, for future reference. |

| Contact Customer Service | Reach out to the new servicer’s customer service for any clarifications or concerns regarding your loan transfer. |

| Gradually Adjust to New Servicer | Familiarise yourself with the new servicer’s policies, procedures, and any additional services they offer. |

Comparison Between Different Banks For Transfer Of Student Loans

When exploring options to transfer student loans, it’s essential to compare offerings from various banks to find the most suitable terms for your financial needs. The table below provides a comprehensive overview of key criteria such as interest rates, repayment terms, eligibility requirements, and additional features for top financial institutions of India.

| Bank Name | Eligibility | Documents Required |

| Axis Bank | – Borrower’s credit score is crucial; higher scores improve chances of approval. – Repayment history on existing loans will be evaluated. – Transfer amount depends on outstanding balance. | – Completed Axis Bank education loan transfer application form. – KYC documents (Aadhaar, PAN, etc.). – Existing loan documents. – Academic documents. – Income proof of co-applicant. |

| SBI | – Must be a legal adult (18 years or older). – The loan must be fully disbursed with regular EMIs paid. – Maximum transfer amount of INR 1.5 crore from other banks. | – Duly filled loan application form. – 2 passport-size photographs. – PAN and Aadhaar cards of student and co-applicant. – Proof of identity (e.g., Driving License). – Proof of residence. – Last 6 months’ bank statement. – IT return of co-applicant for last 2 years (if applicable). – Statement of assets and liabilities of a co-applicant. – Proof of income (salary slips/Form 16) of a co-applicant. |

| HDFC Credila | – Credit score is important; higher scores improve approval chances. – Repayment history on current loans will be assessed. – Minimum income requirements may apply. | – Fully filled balance transfer application form. – KYC documents (Aadhaar, PAN, Driving License, etc.). – Fee repayment receipts from existing lenders. – Any additional documents requested by HDFC Credila. |

Transferring your education loan in 2025 can be a smart financial move, offering the chance to lower interest rates, extend repayment periods, or simplify loan management. However, it’s crucial to carefully evaluate all factors, including transfer fees, new repayment terms, and any potential impact on your credit score. With the right strategy, an education loan transfer can ease your financial burden and help you focus more on your academic and career growth.

FAQs

1. How to transfer an education loan?

To transfer an education loan, your current lender will provide a statement of the pending loan amount. Submit this statement to the new bank for refinancing.

2. Do education loans get rejected?

Yes, education loans can get rejected due to poor academic performance, such as repeatedly failing subjects, not completing the course on time, or scoring below the lender’s minimum required marks (usually 50% or more).

3. Can I transfer my loan account to another bank?

To transfer your loan to a new bank, simply close your loan account with the current lender and pay a transfer fee to the new bank. The new bank will then clear your existing loan, and you can start repaying them through equated monthly instalments at a new rate of interest.

4. Can I transfer my education loan to a lender that offers a lower interest rate?

Yes, you can transfer your education loan to a lender offering a lower interest rate through a process known as loan refinancing or balance transfer.

5. What happens to my student loan if I change university?

You can modify your education loan details, including changing your university, by filling out a form with the new information and submitting it to the bank.

We hope you enjoyed reading this blog! For more helpful tips and insights, explore the links below.

Recent Posts