Table of Contents

One of the government’s main priorities is to ensure that no student misses the chance to learn because of the unavailability of finances. In 2009, a scheme named the ‘Central Sector Interest Subsidy Scheme’ (CSIS) was initiated to meet this goal by the Ministry of Human Resource Development (MHRD) to increase interest subsidies for educational loans.

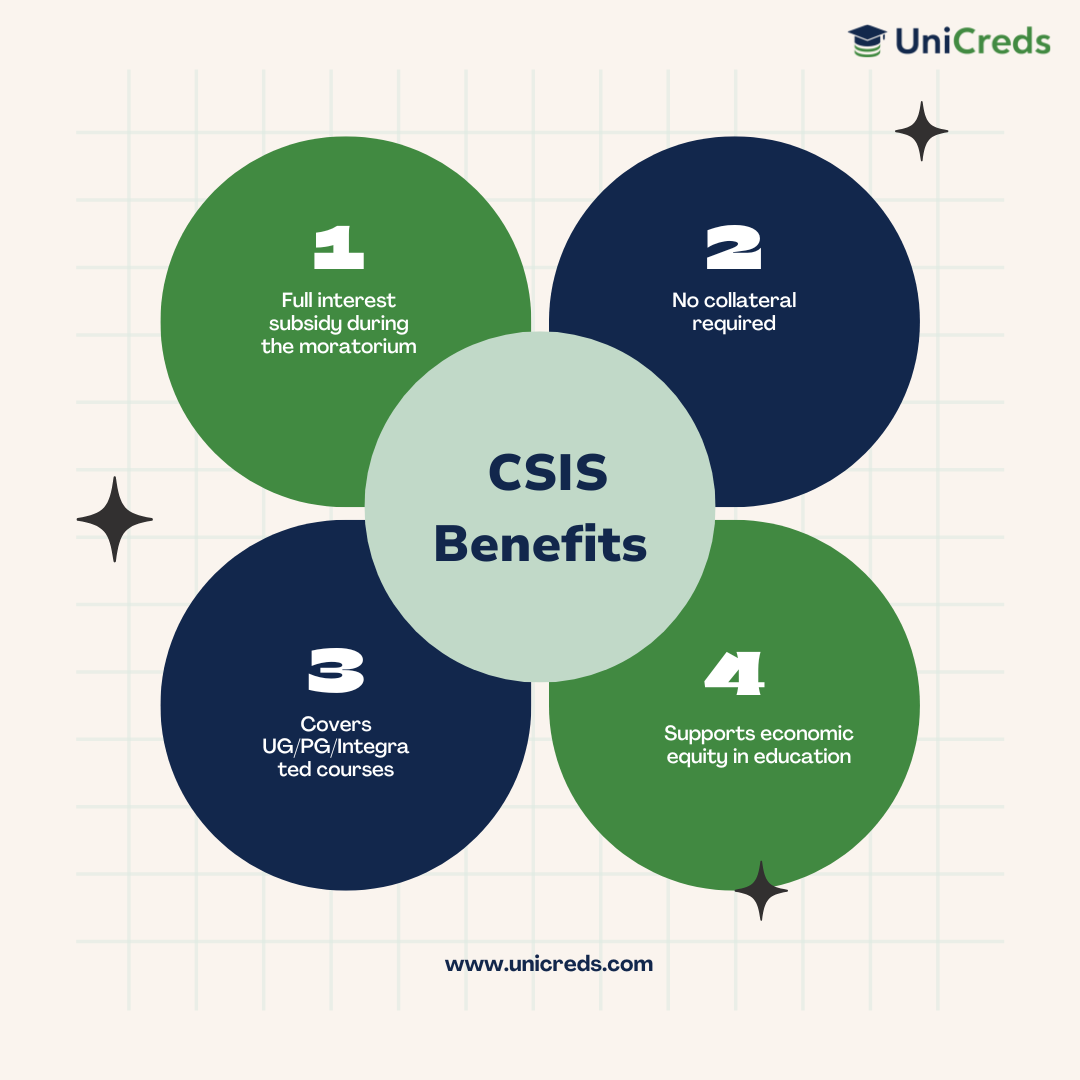

During the moratorium on modern training loans without collateral protection and without third-party guarantee, the programme offers full interest subsidies for education loans to aspirants of technical/professional training in India. The scheme makes students with annual parent/family gross income of up to Rs. 4.5 lakhs. Here’s all you need to know about the education loan interest subsidy scheme.

What Is CSIS Scheme For Education Loan?

The CSIS Scheme aims to provide educational loans to students belonging to the Economically Weaker Section (EWS) with annual family incomes of up to Rs. 4.5 lakhs. The Cabinet recently approved modifications to the existing scheme on January 19th, 2022, emphasising the government’s dedication to enhancing accessibility and affordability in education.

The table given below consists the key features of the CSIS:

| Interest Subsidy On Educational Loans For Overseas Studies Overview | |

| Features | Details |

| Maximum Loan Amount Eligible for Interest Subsidy | Up to Rs. 10.0 lakh |

| Eligibility for Interest Subsidy | Undergraduate, postgraduate, integrated course (graduate + postgraduate) |

| Security Required | No collateral security or third-party guarantee required |

| Credit Guarantee Fund Scheme for Education Loan (CGFSEL) | For loans up to Rs. 7.5 lakh, the beneficiary’s bank shall guarantee coverage for the CGFSEL guarantee. |

| Moratorium period | Course Duration + 1 year |

| Interest Rates | In accordance with the BPLR/Base Rate of each individual bank and the rules for interest rates under the IBA Model Educational Loan Scheme |

Types Of Interest Subsidy Scheme For Education Loan Abroad

The Central Sector Interest Subsidy Scheme (CSIS) has been adopted by all Scheduled Banks, Regional Rural Banks (RRBs), and Cooperative Banks across India. This initiative is designed to motivate students to begin their education at the foundational level and increase the number of skilled technicians and professionals nationwide. CSIS aims to tackle the existing regional imbalance in Gross Enrollment Ratios (GER) among higher education institutions. Given below are the types of Central Government Education Loan Subsidy Schemes adopted by many financial institutions in India:

Padho Pardesh Scheme

The Indian government’s Ministry of Minority Affairs has implemented the Padho Pardesh Scheme, to support academically inclined students from marginalised communities. Under this programme, the Government of India takes on the responsibility of covering the interest on education loans taken by students during the period of moratorium in order to give them a low-interest in education loans.

| Eligibility | Features |

| – Indian citizens – Admission in approved Master’s, M.Phil., or PhD. level courses – Loans from scheduled bank under Indian Banks Association Education Loan Scheme – Application submitted within first year of course – Combined annual income of applicant and guardian/parent not exceeding Rs. 6 lakhs | – Interest coverage during course duration + 1 year or 6 months post-employment – Loans for studying abroad – Applicable to students from minority communities – Eligible for Master’s, M.Phil., and PhD. programs – Exclusivity clause against other government educational loan subsidies |

Central Sector Interest Subsidy Scheme For Education Loan

The Central Sector Interest Subsidy Scheme for Education Loan is a program implemented by the Indian government to provide financial assistance to students pursuing higher education.

Here are the key details of the scheme:

| Features | Eligibility |

| – Government covers interest on education loans during moratorium period – Moratorium period = course duration + 1 year – No collateral required – No third-party guarantee needed – Applicable to professional and technical courses in India – Maximum loan amount: Rs. 7.5 lakh | – Loans obtained through the Indian Banks Association Education Loan Scheme – Parental annual income ≤ Rs. 4.5 lakh – Courses in professional or technical fields accredited by NAAC or NBA – Approval required for non-accredited courses or institutions – Applicable to undergraduate, postgraduate, and integrated courses – Eligibility based on economic index, not social background |

Dr. Ambedkar Central Sector Scheme of Interest Subsidy for Educational Loans

The Ministry of Social Justice and Empowerment, under the Government of India, administers a program that provides interest subsidies on education loans to both Other Backward Classes (OBC) and Economically Backward Classes (EBC). This initiative aims to support students from these disadvantaged backgrounds in pursuing their educational aspirations.

| Features | Eligibility |

| – Applicable for both domestic and international courses – Education loans under the Indian Banks Association Education Loan Scheme – Collaboration between National Backward Classes Finance & Development Corporation and banks – Government interest subsidies during the course or moratorium period – Applicable for Masters, M.Phil., and PhD. levels | – Total annual income ≤ Rs. 8 lakh for OBC category and ≤ Rs. 2.5 lakh for EBC category – Indian citizenship |

Overall CSIS Loan Eligibility Criteria

To qualify for the CSIS subsidy scheme, applicants must meet specific fundamental eligibility criteria set forth by the Indian Government.

Here are the essential requirements:

- Education loans must be obtained under the IBA Model Education Loan Programme.

- Eligibility is restricted to EWS candidates, whose parental or family income (from all sources) does not exceed 4.5 lakhs per annum.

- The scheme applies to Technical or Professional courses offered by NAAC, NBA, and CFTI accredited institutions in India.

- Courses not accredited by NAAC or NBA must receive endorsement from their respective regulatory bodies. For instance, medical, nursing, and law courses require approval from the Medical Council of India, the Nursing Council of India, and Bar Council of India, respectively.

- The interest subsidy is available to eligible students pursuing their first undergraduate or postgraduate degree/diploma in India. However, it’s important to note that the subsidy is a one-time benefit.

- Integrated courses (combining undergraduate and postgraduate studies) are also eligible for the interest subsidy.

- To avail of the interest subsidy, students must complete their course without discontinuation or expulsion from the institution due to disciplinary or academic reasons. In case of discontinuation due to medical reasons, students may still qualify for the subsidy by providing necessary documentation to the Head of the educational institution.

Eligible Courses Under CSIS Education Loan

The list of courses eligible for a CSIS Education Loan is an extensive compilation of educational programmes and disciplines that meet the criteria for financial aid under the CSIS scheme. The table below consists of the list of eligible as well as non-eligible courses under this scheme:

| List of Eligible Courses Under CSIS | List Of Non-Eligible Courses Under CSIS |

| -UG and PG courses in Engineering (B.E. /B.Tech /M.Tech /B.Arch /M.Arch, etc.) -Medical /Para Medical (MBBS /MD /B.sc /M.sc /Nursing /B.Pharmacy /M.Pharmacy /BPT /MPT /BOI /MOI /Siddha /Ayurveda /Homeopathy /Naturopathy, etc.) -Agriculture (B.sc /M.sc)VeterinaryLaw Dental (BDS /MDS) -Management (BBA /MBA) -Computer (BCA /MCA) | -Any courses Abroad Courses pursued without completing class 12th -Non- professional and non-technical UG and PG courses in Arts, Science, Commerce, Sociology, Music, etc. -Diploma courses (except PG Diploma) -Teacher Training courses Skill Development courses Vocational Training courses, etc. |

Documentation Needed For CSIS Education Loan Subsidy

When applying for the CSIS scheme, certain documents are essential to verify eligibility and facilitate the loan process. These documents serve as crucial evidence of the applicant’s qualifications, financial status, and enrollment in eligible educational programmes.

- For CSIS, an income certificate and a loan agreement are required.

- For ACSIS, an income certificate and a caste certificate issued by a competent authority are necessary.

- For the Padho Pardesh Scheme, an income certificate and a minority certificate issued by a competent authority are mandatory.

- For all bank-based subsidy schemes, applicants must provide an income certificate, valid ID proofs, and proof of admission.

How To Apply For Central Interest Subsidy Scheme?

Understanding how to apply for the Interest Subsidy Scheme for education loan abroad is crucial for those seeking financial support for their education. This scheme aims to ease the burden of educational expenses, providing valuable assistance to students.

Knowing the application process ensures that eligible individuals can access the benefits of the scheme smoothly, making their educational pursuits more manageable.

Step 1: Head to the official website or connect with the UniCreds loan experts, to understand about the various available loan schemes catering to students.

Step 2: Select the ‘Scheme’ option from the menu, presenting multiple choices; opt for ‘Education Loan.’

Step 3: Within the Education Loan section, explore the options and locate ‘Central Sector Interest Subsidy (CSIS).’

Step 4: Access the detailed description of eligibility criteria either on the website or refer to this article for comprehensive information.

Step 5: Towards the end of the page, locate and click on the ‘Check Eligibility’ option.

Step 6: Complete all required fields, including location of study, Gross family annual income, Social category, Course length, Course Type, Course fees, and personal investment amount, then click ‘Check Eligibility.’

Step 7: Upon submission, receive information on Eligible Subsidy Amount, Monthly EMI, and Loan Tenure.

Step 8: Proceed by clicking on the ‘Apply Now’ option.

Step 9: Stay updated on your application progress by selecting the ‘Track Your Application’ option.

Did you know?

There are scholarships that offer interest-free loans for students, allowing them to repay over an extended period? Some of these loans even offer forgiveness based on academic performance. Discover more scholarship opportunities for Indian students and receive regular updates via SMS and email on our website.

In conclusion, the Central Sector Interest Subsidy (CSIS) Education Loan Scheme stands as a beacon of hope for countless aspiring students across India. With its commitment to providing financial support to economically disadvantaged students pursuing higher education, CSIS embodies the government’s dedication to fostering a brighter future for the nation.

FAQs

1. What are the rules for education loans?

The repayment period for the loan is set at 5-7 years, which begins after the commencement of repayment. In cases where the student is unable to complete the course within the designated timeframe, an extension of up to 2 years may be granted for the completion of the course.

2. Can we take an education loan two times?

Certainly, it is possible to obtain a second education loan, given that you fulfil the requirements for the second loan. You have the flexibility to choose whether you would like to obtain the loan from the same bank where you previously obtained your graduation loan or explore options with a different lender.

3. What is the limitation of an education loan?

Banks conduct a thorough evaluation of the academic record of the candidate, expecting a consistently strong performance throughout the course to ensure timely repayment of the loan. It should be noted that educational loans typically carry a relatively high-interest rate.

4. How many days are required to sanction an education loan?

It takes 7 working days to sanction a student loan.

5. What happens if an education loan is not paid?

In the event of non-payment of an education loan in India, the lender will initiate a series of notices to both the borrower and the guarantor. Failure to respond or take necessary action will result in loan default, significantly impacting your credit score. As a consequence, obtaining any future loans may become challenging for an extended period.

6. Is there any subsidy on education loans for abroad studies?

Schemes like the Padho Pardesh Scheme offer subsidies for education loans for studying abroad.

7. What is the interest rate for education loans in Indian Overseas Bank?

The education loan interest rate for education loans in Indian Overseas Bank ranges between 11-12%.

8. How can I check my education loan subsidy status?

You can click on the ‘track your application’ option on the website to check your education loan subsidy status. You can also check with a UniCreds representative on this!

9. Is there any income limit to qualify for the Education Loan Interest Subsidy Scheme?

Yes, for the Education Loan Interest Subsidy Scheme, the income limit is set at Rs. 4.5 lakhs per annum for economically weaker section (EWS) applicants.

10. What is the maximum subsidy provided under the Education Loan Interest Subsidy Scheme?

The maximum subsidy provided under the Education Loan Interest Subsidy Scheme is the interest on education loans for the duration of the course plus one year or six months after securing employment, whichever comes first.

11. Can existing education loan borrowers avail of the Education Loan Interest Subsidy Scheme retroactively?

No, existing education loan borrowers cannot avail of the Education Loan Interest Subsidy Scheme retroactively.

Popular Loans

Student loans USA | Education loan to study in UK | Study loan for Canada | Ireland student loan | Education loan for studying in Australia | Student loan for New Zealand

")

")

{kind=link}

0 Comments