Table of Contents

You’ve got your dream university offer in hand. The excitement’s real, but so is the big question—how do you fund it?

Tuition, accommodation, flights, daily expenses… adds up super fast.

An education loan seems like the best option, but then comes the real challenge: secured vs unsecured loans. Which one to choose? Which one suits your financial situation?

Simply put, a secured loan requires collateral—such as property or fixed deposits—for lower interest rates.

On the other hand, an unsecured loan doesn’t need collateral, but it might have stricter terms.

Let’s break it down, step by step, with clear insights so you can make a choice that fits your future and your finances.

Difference Between a Secured and Unsecured Education Loan

Choosing the right education loan can feel overwhelming, especially when faced with two options—secured and unsecured loans. Both have benefits and trade-offs, but which one suits you best?

Here’s a side-by-side comparison to make your decision easier:

| Criteria | Secured Loan | Unsecured loan |

| Collateral Requirement | Needs collateral like property, FD, or insurance. | No collateral is required. Approval depends on credit history and the co-borrower’s financial standing. |

| Interest Rates | Lower, since the lender has security. | Higher, as there’s more risk for the lender. |

| Loan Amount | Can be higher, depending on the collateral’s value. | Usually lower, based on your financial profile. |

| Eligibility Criteria | More relaxed, as collateral reduces risk. | Stricter, focusing on creditworthiness and repayment ability. |

| Processing Time | Longer due to property verification and documentation. | It’s faster since there’s no collateral to assess. |

| Repayment Terms | Typically, longer repayment periods. | Shorter repayment terms with stricter conditions. |

When choosing an abroad education loan, you’re not just picking between secured and unsecured options. There’s also a middle ground—partially secured loans.

Also called unsecured loans, they allow you to pledge collateral of lesser value than the total loan amount. The remaining portion is treated as an unsecured loan.

Now that we’ve outlined the key differences between secured and unsecured education loans let’s delve deeper into the specifics of secured loans for overseas students.

What is a Secured Loan for Studying Abroad?

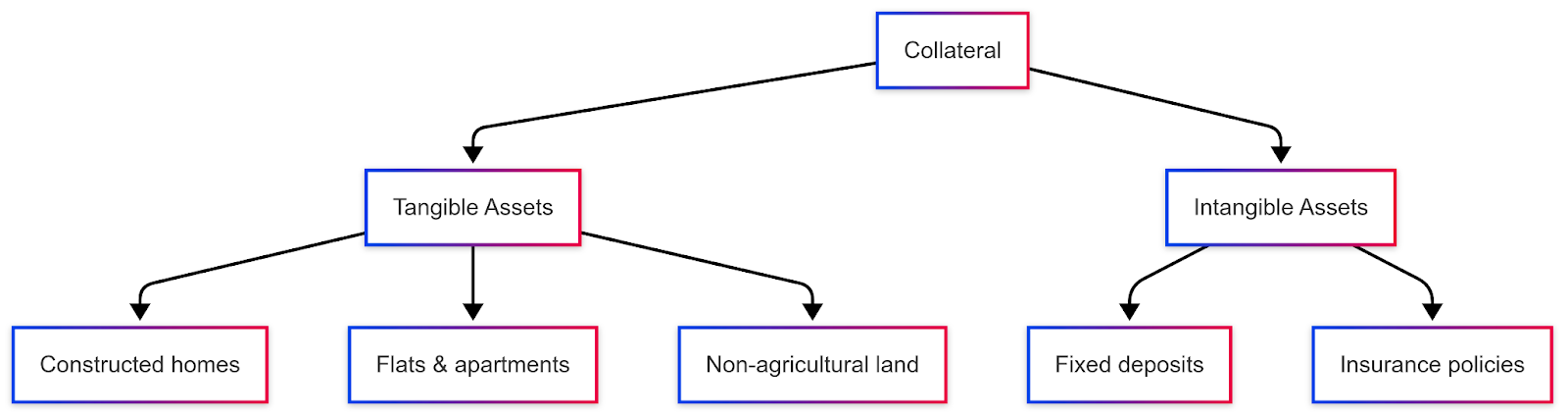

A secured loan to study abroad is where you pledge collateral—such as property, fixed deposits, or insurance—to get funding for your studies.

Since the lender has security, they offer lower interest rates and higher loan amounts. This makes secured loans a great choice if you or your family own valuable assets.

Key Features of Secured Education Loans

- Collateral is mandatory – You need to pledge property, fixed deposits, or other assets.

- Lower interest rates – Lenders charge less since they have security.

- Higher loan amount – Can cover tuition, living expenses, and more.

- Longer repayment period – Usually, you get more time to repay.

- Approval depends on collateral value – Your asset’s worth affects how much you can borrow.

- Preferred by public sector banks – Most government banks offer secured loans.

Understanding Collaterals

A collateral is an asset that you pledge to secure a loan. Regarding education loans, collateral can be either a physical or financial asset.

How Much Collateral Do You Need?

Most banks want collateral worth at least 125% of your loan amount. But this isn’t a fixed rule.

Depending on their policies, some lenders may ask for less, while others might need more.

Your profile plays a significant role in this decision. Banks don’t treat all applications the same—they evaluate each one differently based on several factors.

Here’s what they consider:

- Your academic performance – A strong track record may work in your favour.

- Loan amount and tenure – Higher loans or longer repayment periods might need stronger security.

- Creditworthiness of you and your co-borrower – A good credit history can be an advantage.

- Ranking of your chosen international university – Top institutions can sometimes make approval easier.

Each case is unique, so it’s always best to check with the bank for exact requirements.

Weighing the Pros and Cons of Secured Loans

| Advantages | Disadvantages |

| Lower than unsecured loans, making repayment easier. | Interest rates may vary based on collateral type and lender policies. |

| Higher loan amounts, covering tuition, living expenses, and other costs. | Limited to the value of your pledged asset. |

| Longer tenure, reducing monthly EMI burden. | If you default, the lender can take legal action on your collateral. |

| Easier approval if you have a strong asset. | Requires property or financial assets, which not everyone has. |

| More chances of approval due to security. | Longer approval time due to collateral verification. |

Should You Consider a Secured Education Loan?

A secured education loan can be a great option. But here’s when it makes sense for you:

- You or your family own a valuable asset to pledge as collateral.

- You want a lower interest rate and a higher loan amount.

- You prefer more extended repayment periods to reduce monthly EMIs.

- You’re comfortable with the time-consuming approval process.

In contrast to secured loans, unsecured education loans don’t require you to pledge any assets. Let’s explore the details of this type of financing.

What is an Unsecured Loan For International Education?

An unsecured education loan helps you study abroad without pledging any collateral.

Banks and NBFCs approve these loans based on your academic record, university ranking, and co-applicant’s financial profile.

Key Features of Unsecured Education Loans

- No Collateral Required – You don’t need to pledge property, fixed deposits, or any other asset.

- Approval Based on Profile – Your academic record, university ranking, and co-applicant’s income play a key role.

- Higher Interest Rates – Since there’s no security, lenders charge higher interest rates compared to secured loans.

- Limited Loan Amount – Loan limits vary depending on your university and lender policies.

- Shorter Repayment Period – Repayment tenure is generally shorter than secured loans, leading to higher EMIs.

- Requires a Strong Co-applicant – A financially stable co-applicant (parent/guardian) improves your chances of approval.

Weighing The Pros and Cons of Unsecured Loans

| Advantages | Disadvantages |

| No need to pledge assets, making it accessible for more students. | Higher interest rates increase the overall repayment amount. |

| Faster approval process helps meet university deadlines. | Loan amounts may be limited based on university ranking and borrower profile. |

| Covers tuition, living expenses, travel, and other academic costs. | Shorter repayment periods result in higher monthly EMIs. |

| Ideal for students accepted into top-ranking universities. | Requires a strong financial co-applicant with a stable income. |

Should You Consider an Unsecured Education Loan?

If you don’t own assets to pledge but have a strong academic record and a financially stable co-applicant, an unsecured loan can be a good option. However, you should be prepared for higher interest rates and shorter repayment tenures. You may get better loan terms if your university ranks among the top institutions. Weigh the costs and repayment burden before making your decision.

So, you plan to obtain an education loan for your studies abroad. But where do you start? Let’s look at some of the top lenders in this space who offer secured and unsecured loans.

Best Loan Providers for Studying Abroad: Banks, NBFCs & More

Choosing the right lender can significantly impact your study abroad journey.

Banks, NBFCs, and international lenders offer secured and unsecured international education loans. Each has its own set of terms, interest rates, and benefits.

Here’s a quick breakdown of your options:

| Public & Private Banks | NBFCs | International Lenders | |

| Loan Type | Secured & Unsecured | Mostly Unsecured | Mostly Unsecured |

| Ideal For | Students seeking lower interest rates & long tenures | Students needing quick approval & flexible terms | Students at top universities needing foreign currency loans |

| Key Considerations | Requires collateral for higher loan amounts | Higher interest rates than banks | Strict eligibility, repayment in foreign currency |

| Examples | SBI Bank of Baroda ICICI Axis Bank | Credila Avanse InCred | Prodigy Finance MPOWER Financing |

Each lender has different processing times, interest rates, and eligibility criteria. Compare your options carefully before making a choice.

With several lenders in mind, how do you make the best choice?

Let’s look at what to consider.

Picking the Right Lender

The best lender depends on your financial situation, loan amount, and repayment ability. Here’s how to decide:

- Public Sector Banks

Have collateral? Public banks offer lower interest rates, higher loan amounts, and tax benefits.

- Private Banks

No collateral but a strong co-applicant? Private banks offer better rates than NBFCs, faster processing, and sometimes even zero-margin loans.

- NBFCs

Struggling with private bank eligibility? NBFCs are more flexible and offer loans up to ₹75 lakh, though at slightly higher interest rates.

- International Lenders

No co-applicant and need a loan? If your university is on their list, international lenders can help. However, expect higher interest rates, USD disbursement, and no tax benefits.

Wrapping Up!

So, what’s your best bet—secured or unsecured loan?

If you have collateral, a secured loan keeps interest rates low and savings high. No collateral? An unsecured loan still gets you there, but at a price.

The real question isn’t just about getting a loan—it’s about getting the right one for your future.

Think long-term. What works for you today should also make sense when repayment kicks in.

Study bright, borrow smart, and set yourself up for success. Your dream university is waiting—now make sure your loan choice gets you there without regrets.

But with so many lenders, terms, and conditions, making the right choice can get overwhelming.

That’s why UniCreds simplifies the process—connecting you with top lenders, negotiating the best rates, and securing approvals in just 48 hours.

Whether you need a non-collateral loan or a lower interest rate, we’ve got you covered.

FAQs

1. Do you need to pledge collateral for an education loan?

No, it’s not always required. You can choose between secured and unsecured loans when you decide to study abroad. Many lenders in India offer unsecured loans of up to ₹75 lakhs if you have a financial co-applicant who meets their criteria.

2. What’s the final takeaway on secured vs unsecured loans?

Both loan types help you fund your studies, but the right one depends on your financial situation. A secured loan is cost-effective if you have collateral, while an unsecured loan gives you access to funds without security. Choose wisely based on your long-term repayment plan and financial comfort.

3. What is the main difference between secured and unsecured loans?

The key difference is collateral. A secured loan requires you to pledge assets like property or fixed deposits. An unsecured loan doesn’t need any collateral but may come with higher interest rates and stricter conditions.

4. How can you get a lower interest rate on student loans?

To secure a lower rate, compare multiple lenders, choose flexible repayment plans, and check whether the interest is charged flat or reduced. A strong co-applicant can also help you qualify for better rates.

Looking for more insights? Check out our related blogs on education loans and financing options:

")

")

{kind=link}

0 Comments