")

Table of Contents

Have you ever taken a loan and found yourself stuck in financial problems? If yes, this hasn’t happened just with you. Especially newly employed students who have just started their student loan repayment, it can be possible that they may or may not get along well with their new job. Or maybe an unavoidable financial problem might have arisen. At such times, you can always opt for an education loan restructuring instead of worrying about how you can manage your debt and other finances. In this blog ‘Identifying the Benefits of Education Loan Restructuring’, we will identify the benefits of education loans.

Meaning Of Education Loan Restructuring

Education loan restructuring means modifying the existing student loan to make it more manageable to repay. It involves changing one of the following:

- Extending the loan term: This method increases the repayment period of the loan term, which reduces the EMI amount but increases the interest rate over the total loan tenure.

- Interest Rate Reduction: You can negotiate for lower interest rates, which ultimately reduces the total cost of borrowing and the monthly payment amount.

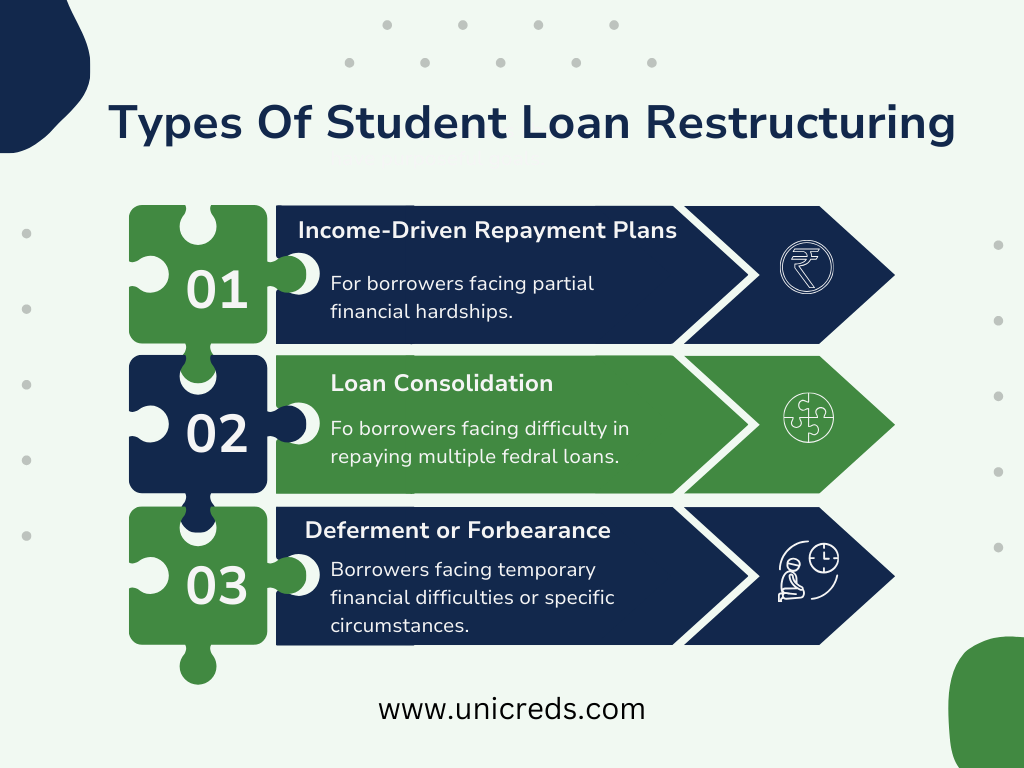

- Change in repayment plan: We are moving to an income-driven repayment plan, where the monthly payment is calculated based on the borrower’s income and family size.

- Loan consolidation: Taking out one loan to pay off multiple student loans, potentially lowering interest rates and extending repayment terms.

Benefits Of Education Loan Restructuring

Reserve Bank of India guidelines say student loan benefits after restructuring help borrowers in financial trouble. Take a look at the benefits of renegotiating your education loans.

- If an education loan is restructured, a moratorium can be placed on it for up to two years.

- Extending the loan tenure to reduce the EMI payable according to the borrower’s repayment capacity is possible.

- The loan restructuring is beneficial in terms of reducing the borrower’s overall debt burden.

- You can transfer the outstanding amount to another credit card.

- Within 90 days, you can implement the loan restructuring plan.

- The loan can be repaid according to your financial situation.

- A more extended repayment period means fewer EMIs to pay each month.

- A restructured education loan can also be restructured with a lower EMI, lowering the overall amount owed.

- You can improve your credit score by paying on time and managing your money wisely.

- Credit scores are affected by loan restructuring, but it’s temporary, and it eventually improves.

Eligibility For Education Loan Restructuring

There are different types of education loan restructuring. So, the specific eligibility criteria may differ depending on the type. Here are the types of education loan restructuring:

Reserve Bank of India guidelines say you can only restructure your loan once during the term. This changes the repayment terms for MSME and corporate borrowers affected by COVID-19. Any personal loan can be restructured for individual borrowers. The RBI approved loan restructuring only for loans that haven’t been outstanding for 30 days. MSME borrowers have an exceptional period of 89 days.

Process Of Education Loan Restructuring

The process of education loan restructuring typically involves the following steps:

1) The first step is to contact the company that services your student loans, either the lender or a third-party servicer. Tell them about your current financial situation and your interest in restructuring.

2) Your bank will probably request documentation to verify your income, expenses, family size, and overall financial circumstances.

3) Based on your information, the bank will assess your eligibility for various repayment plan options. These may include:

- Income-driven repayment plans (e.g., IBR, PAYE, REPAYE)

- Extended repayment terms

- Loan consolidation

- Deferment or forbearance

4) After reviewing the options, you must select the restructuring plan that best suits your needs and financial situation.

5) Once you’ve chosen a restructuring plan, you must complete and submit the required paperwork and wait for your loan restructuring to get approved.

Documents Required For Education Loan Restructuring

Different documents may be needed depending on what restructuring option you’re selecting (e.g., income-driven repayment plan, consolidation, deferment, or forbearance). During the restructuring process, your loan servicer will give you a list of what you need. Here are the general documents typically required for education loan restructuring, presented in a table format:

| Document | Description |

| Income Documentation | -Recent pay stubs or wage statements (typically for the last 3–6 months) -Federal income tax returns (generally for the most recent tax year) -Proof of other sources of income (e.g., child support, alimony, disability benefits) |

| Family Size Documentation | -Federal income tax returns or transcripts showing family members claimed as dependents – Birth certificates or adoption papers for dependent children – Marriage certificate or divorce decree (if applicable) |

| Loan Documentation | – Loan statements or letters from your loan servicer(s) showing your current loan balance(s), interest rate(s), and monthly payment amount(s) |

| Expenses Documentation | – Recent utility bills (electricity, gas, water, etc.) – Rent or mortgage statements – Insurance premiums (health, auto, etc.) – Credit card statements or other loan statements |

| Identification Documents | – Government-issued photo ID (driver’s license, passport, etc.) – Social Security card or other official document with your Social Security number |

| Proof of Circumstances (if applicable) | – Letter from your employer regarding job loss, reduction in hours, or change in income – Medical bills or documentation of disability or illness – Military orders or deployment documentation (for active duty service members) |

Tips To Avoid Student Loan Restructuring

Why go through the entire process of restructuring when you can manage your finances well? Here are some tips to avoid a financial crisis and repay loans without any problems in the future:

- Borrow only what is needed. You should carefully consider your future income and then borrow the loan amount that’s necessary to cover tuition fees, living expenses, etc.

- Track your expenses and prioritise saving the most money. You can even opt for internships or part-time jobs to gather emergency funds in case of financial crisis.

- Start repaying early if possible. You can repay small amounts towards your loan by utilising the internship stipends or the money saved at the end of every month.

- Keep upskilling throughout your education to secure a good job placement with a higher salary. This way, you won’t fall short of funds.

That’s it! I hope this blog helped you identify the benefits of education loan restructuring and how you can manage your finances well as an alternative. For more such advice, you can contact UniCreds!

FAQs

Q1. What is the purpose of loan restructuring?

The purpose of loan restructuring is to modify the repayment terms of a loan in favor of the borrower, reducing debt pressure with lower interest rates, a longer repayment period, or deferment.

Q2. What will happen if I restructure my loan?

You can pay the loan on an extended loan tenure or reduced interest rates.

Q3. Is loan restructuring good for borrowers?

Yes, loan restructuring is suitable for borrowers facing a partial or temporary financial crisis.

Q4. Is there a processing fee I must pay if I restructure my loan?

You may be levied a fee if you apply to get your loan restructured.

Q5. Can I remove the loan restructure status from my CIBIL report?

When you make regular payments and monitor your CIBIL report, you can quickly remove the loan structure status.

Q6. Does loan restructuring impact Credit score?

Loan restructuring indeed affects credit scores. It indicates a problem with making payments that may lead to lenders barring you.

Q7. How does loan restructuring impact credit score?

According to the loan structure, there is a crisis in making payments, which could lead to lenders barring them.

")

")

{kind=link}

0 Comments