Table of Contents

You thought the hard part about studying abroad was picking a country, or maybe cracking the IELTS. But no one cleared the air about credit score ranges.

Then one day, your loan agent casually drops the word “CIBIL,” and you wonder if they are asking about your score or your parents’? What if it’s too low? What does “too low” even mean?

Most students reach this point unsure of what the score means, why it matters, or how it affects their loan. And it’s easy to assume the bank will “take care of it.” But your credit score (or your co-applicant’s) could decide how soon your loan gets approved, or if it does at all.

This blog will help you understand what credit score ranges mean, how they work in student loan applications, and what you can do right now to make the process smoother.

What Is a Credit Score In Education Loans?

When you apply for an education loan, the lender wants to know one key thing: Can you pay it back? That’s where your credit score comes in. A credit score is a number that shows your financial reliability based on your past borrowing and repayment behaviour.

In India, the most common credit score you’ll hear about is the CIBIL score. This three-digit number ranges from 300 to 900. The higher your score, the more trustworthy you appear to banks and lenders. For education loans, your credit score ranges matter a lot because they influence loan approval and the interest rates offered.

The best CIBIL score range usually starts around 750 and above. Scores in this range tell lenders you manage your finances responsibly. You might face higher interest rates or stricter loan conditions if your score falls below this.

Importance of CIBIL Score in an Education Loan Abroad

- Shows Your Financial Responsibility to Lenders

Your credit score range gives lenders a snapshot of how well you’ve handled credit in the past. Since many students don’t have a credit history, lenders rely heavily on this number to judge whether you can repay your loan on time. A solid score reduces doubts about your financial habits.

- Affects Loan Approval Chances and Terms

The best CIBIL score range starts around 750. Scores in this range signal low risk, making lenders more willing to approve your loan. If your score is lower, your application might face delays or even rejection. Even if approved, you’ll likely pay higher interest rates, increasing your loan’s overall cost.

- Co-applicant’s Score Is Crucial When You Lack Credit History

Most students applying for education loans abroad don’t have enough credit data. That’s why your co-applicant, usually a parent or guardian, plays a big role. Their credit score directly impacts your loan approval and interest rates. A strong co-applicant score can balance out your limited history.

- Determines the Loan Amount and Repayment Flexibility

Lenders consider credit scores to decide how much money they’re willing to lend. A higher score often means access to larger loans, helping cover tuition, living expenses, and other costs abroad. It can also influence repayment options, letting you choose terms that fit your budget.

- Timely Loan Repayments Build a Better Credit Profile

Once your loan is active, paying EMIs on time improves your credit score, which benefits future borrowing. Missing payments harms your score, making it tougher to secure credit later, for example, for a car or home loan after your studies.

- Knowing Your Score Helps You Prepare and Improve Before Applying

Understanding your credit score ranges early gives you time to fix errors, clear dues, or build a positive record. This preparation boosts your chances of loan approval and can help you negotiate better terms.

What CIBIL Score Do You Need for an Education Loan Abroad?

When you apply for an education loan to study abroad, lenders look closely at your credit score range to decide your eligibility.

The best CIBIL score range improves your chances of approval and better loan terms. Since many students have little or no credit history, lenders often check the co-applicant’s score.

Here’s a guide on what scores lenders expect:

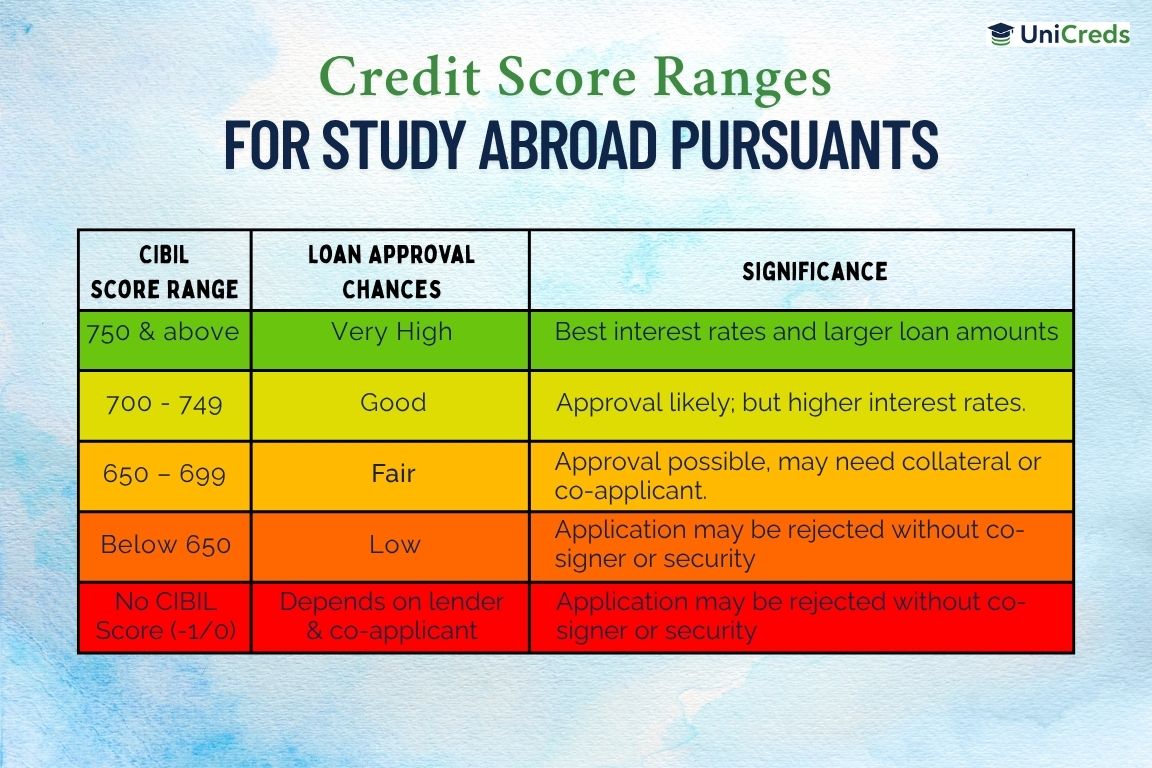

| CIBIL Score Range | Loan Approval Chances | What It Means for You |

| 750 and above | Very High | You qualify for the best interest rates and larger loan amounts. |

| 700 – 749 | Good | Loan approval likely; interest rates may be slightly higher. |

| 650 – 699 | Fair | Loan approval is possible but may need collateral or a strong co-applicant. |

| Below 650 | Low | Loan application may be rejected without additional security or co-signer. |

| No CIBIL Score (-1/0) | Depends on lender and co-applicant | Lenders may consider income, collateral, or co-applicant’s credit standing. |

Key Points to Remember:

- Most private lenders want a CIBIL score of 700 or above for education loans abroad.

- The best CIBIL score range (750+) opens doors to flexible loan amounts and lower interest rates.

- Government banks may accept lower scores but expect stricter documentation.

- A co-applicant with a strong credit history can make a big difference if you lack a credit score.

- Some lenders, especially NBFCs, may accept scores from 650 for professional courses, but conditions apply.

Knowing where you stand in these credit score ranges helps you prepare better for your loan application. It also guides you in improving your credit profile or choosing the right co-applicant for your loan process.

Wondering how your credit score affects your study abroad loan?

Regardless of your credit score, we have the right loan options for you. Apply now for an abroad education loan and start your abroad journey today!

Is Your Co-Applicant’s CIBIL Score Important?

When you apply for an education loan, you might not have much credit history yourself. That’s why lenders often look at the CIBIL score of your co-applicant. Usually, this is a parent, guardian, or spouse who supports your loan application.

Your co-applicant’s credit score range can make a big difference. If their score falls within the best CIBIL score range, around 750 or higher, it shows the lender they’re financially responsible. This improves your chances of getting the loan approved quickly and with better terms.

If the co-applicant’s score is below 700, lenders may ask for collateral or charge higher interest rates. That can make the loan more expensive and harder to manage. So, picking a co-applicant with a strong credit score is one of the smartest moves you can make.

Ultimately, your co-applicant’s credit score carries weight shaping how much you borrow and the conditions you get.

Bank-Specific CIBIL Score Requirements for Study Abroad Loans

When you apply for a study abroad loan, each bank sets its own credit score ranges for approval. Knowing these helps you target the right lender and improve your chances.

Public Sector Banks

- State Bank of India prefers applicants with a CIBIL score of at least 700. They offer loans up to ₹1.5 crores covering tuition and living expenses abroad.

- Bank of Baroda looks for a minimum score of 700 and provides comprehensive loan packages that include course fees and other costs.

- Canara Bank shows flexibility with credit scores when co-applicants have strong financial backgrounds, easing the process for many students.

Private Banks

- Credila seeks the best CIBIL score range, usually 750 or above, rewarding high scores with faster processing and better terms.

- ICICI Bank recommends a minimum score of 700 and offers a fully digital application experience, making it easy to apply from anywhere.

- Axis Bank requires a score above 700 and provides collateral-free loans up to ₹40 lakhs for students enrolled in top universities abroad.

Understanding these specific requirements lets you focus on improving your credit score or choosing a suitable co-applicant. This way, you can apply with confidence and avoid unnecessary delays.

Smart Ways to Build a Strong Credit Score Before You Apply

Lenders check credit score ranges to judge if you (or your co-applicant) are dependable borrowers. If your score isn’t in the best CIBIL score range, your chances of getting favourable terms, or any loan, drop quickly.

If You Have No Credit History Yet

- Start Small With a Student Credit Card

Apply for a basic credit card from the bank your parents already use. Most banks issue entry-level cards with low limits to students or guardians. Use it only for essential spends like ₹2,000–₹5,000 a month on groceries or recharge.

Then, always pay the full amount before the due date. Not the minimum due, but the full balance. It shows you can borrow and repay responsibly. Missed payments will cause more damage than having no card at all.

- Stick to the 30% Rule

If your credit limit is ₹10,000, try to keep usage below ₹3,000 at any given time. High credit utilisation signals financial stress. Low utilisation, paid in full, boosts your score over time.

- Get Added as an Authorised User

Your parents or guardians can add you to their credit card as an authorised user. Their good repayment history can reflect positively on your credit report, even if you’re not directly managing the card. This is especially helpful if you can’t get a credit card on your own. Just ensure their credit habits are solid, as their missed payments can hurt your score too.

If You Already Have a Credit Score, But It’s Low

- Clear All Outstanding Dues — ASAP

Outstanding card payments, even small ones, pull your score down. Settle all dues before applying for your education loan. The sooner you pay, the sooner your credit score improves.

- Pay All Bills on Time, Every Time

Late payments stay on your credit record for months. This includes utility bills, EMIs, and even your mobile recharge if it’s postpaid. Use reminders or auto-debit options to never miss a due date.

- Avoid New Credit Products

Don’t apply for multiple loans or cards in a short span. Every enquiry adds a mark to your credit report. Too many applications in one go can make lenders suspicious, even if you’re financially stable.

Securing an Education Loan Abroad with a Low CIBIL Score

Do not panic or lose hope if your CIBIL score isn’t great. A low score doesn’t shut the door. It just means you’ll need to knock harder and smarter.

Many students get their loans approved even with a credit score under 700. Here’s how you can still make it work.

- Offer Collateral for a Secured Loan

This is your strongest move when your score falls short of the best CIBIL score range. You can pledge:

- A residential property

- Fixed deposits

- Life insurance policies

Collateral tells the lender: “I’ve got something at stake.” That reduces their risk and improves your chances, even if your score is below 650.

- Pick a Strong Co-Applicant

Your co-applicant’s score can make or break your case. If your score is low, get someone with a score of 750 or above to sign with you. Parents, siblings, grandparents can apply, as long as they have income proof and a strong repayment record. The better their score, the more confident the lender will be.

- Apply Through Public Banks or Government Schemes

Some government banks are more flexible with credit scores, especially when collateral or co-applicants are involved. You can also check if you’re eligible for schemes like the Central Sector Interest Subsidy (CSIS). These programmes often care more about income and course type than your credit score.

- Explore NBFCs and New-Age Lenders

Private lenders like InCred, Auxilo, and MPower Financing often approve loans for credit scores as low as 650. Instead of just numbers, they look at:

- Your course

- Future earning potential

- University reputation

So if you’re planning a high-return degree (like an MBA or STEM course), this route could work well.

- Show Proof of Repayment Capacity

Even with a low score, your case strengthens if you can prove income stability. Lenders may approve your application if your co-applicant:

- Earns regularly

- Has consistent bank statements

- Holds a job with a reputed employer

They want to see that EMIs will be paid without delays.

Your credit score doesn’t define your ambition. But lenders do check it. So if you’re not in the best CIBIL score range yet, give them another reason to say yes.

Checking Your CIBIL Score

When to Check Your CIBIL Score?

- Once Every Three Months

That’s usually enough to catch errors or track progress without going overboard.

- Before You Apply for a Loan

Give yourself time to fix anything that looks off. The best CIBIL score range doesn’t come overnight.

- Right After Big Money Moves

Bought something on EMI? Took a loan? Applied for a credit card? Check your score soon after to spot any dips.

- If You’re Trying to Improve Your Score

Got a low score and actively working on it? A monthly check helps you see what’s working.

How to Check Your CIBIL Score?

- Use the Official CIBIL Website

Visit www.cibil.com You get one free report a year—use it well.

- Explore Credit Tracking Apps

Apps like BankBazaar or PaisaBazaar let you check your score for free with minimal details.

- Check via Your Bank’s App

Many banking apps now offer free credit score checks. They’re fast and easy and don’t count as a hard enquiry.

These checks are called soft enquiries. No matter how often you view it, they won’t hurt your score.

Pro Tip: Set a quarterly reminder. Keep an eye on your score without obsessing over it.

Worried about managing your loan repayments?

Use our Education Loan EMI Calculator to estimate your monthly repayments, regardless of your credit score, and plan your finances better for studying abroad.

A Month-by-Month Plan To Apply for an Education Loan

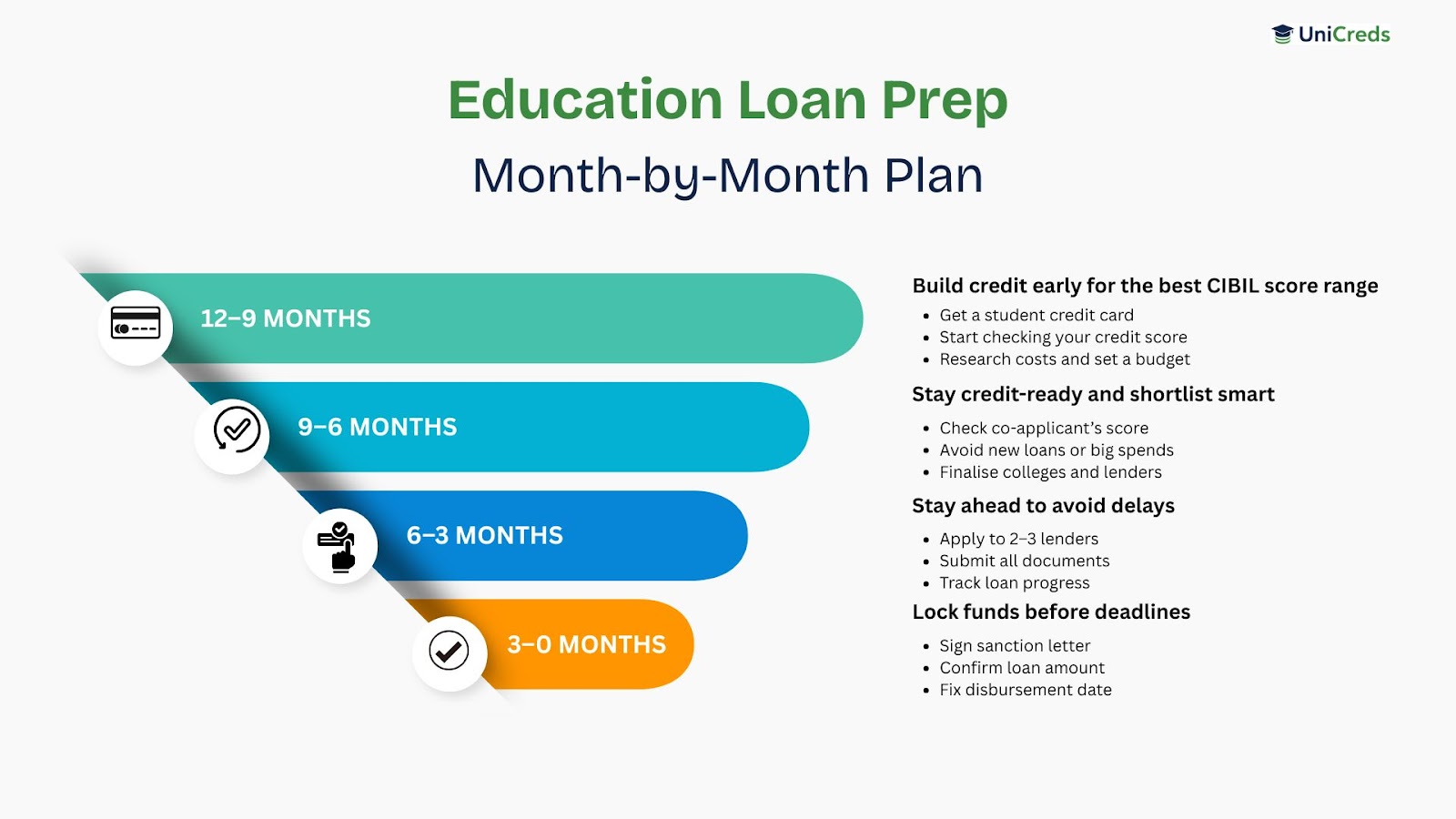

Start early. Stay ahead. The right timing can mean faster approvals, better terms, and less last-minute stress.

Here’s a smart 12-month breakdown to get you started on the right foot.

| Timeline | What to Do | Why It Matters |

| 12 to 9 Months Before Intake | – Apply for a student credit card or get added as an authorised user- Use and repay on time- Start tracking your credit score- Research university costs and plan a budget | Builds early credit history and helps you aim for the best CIBIL score range before applying |

| 9 to 6 Months Before Intake | – Review co-applicant’s credit score- Avoid large spends or new loans- Finalise university choices- Shortlist loan providers (banks, NBFCs, fintechs) | Ensures your co-applicant fits within ideal credit score ranges and helps you narrow down options |

| 6 to 3 Months Before Intake | – Apply to 2–3 lenders- Gather documents: ID, income proof, admission letter, etc.- Follow up for loan status | Timely submission increases approval chances and avoids last-minute delays |

| 3 to 0 Months Before Intake | – Review and sign the sanction letter- Confirm loan amount and coverage- Plan your disbursement schedule | Final steps matter. This locks in your funding before university deadlines |

Wrapping Up

You now know what many students don’t. Credit score ranges show your trustworthiness and shape how lenders see you. The best CIBIL score range won’t improve by chance. But now you understand where to focus your efforts.

This means you’re not just hoping for loan approval, you’re preparing for it, ahead of time and with purpose. So, before you apply, take a moment to check your score. Fix what needs fixing.

And as you build your credit habits, know that UniCreds stands ready to support your loan needs with fast sanctions, competitive rates, and loans without collateral. Your study abroad journey deserves a partner that moves as fast as you do.

FAQs

1. What credit score ranges are required for an education loan to study abroad?

Most lenders prefer a CIBIL score of 700 or above to approve education loans for studying abroad. However, having a score in the best CIBIL score range of 750+ can boost your chances of approval and help you secure better interest rates.

2. Can you get an education loan for studying abroad without any CIBIL score?

Yes, it is possible. If you or your co-applicant has no credit history (CIBIL score of -1 or 0), lenders may still approve the loan by considering collateral, income proof, or future earning potential. NBFCs and fintech lenders like MPower Financing are more flexible in such cases.

3. How important is a co-applicant’s CIBIL score in an education loan application?

Ideally, having a co-applicant with a CIBIL score above 750 significantly increases your loan approval chances. It can also unlock better loan terms such as lower interest rates and higher loan amounts, as banks rely heavily on the co-applicant’s creditworthiness.

4. Do government banks have different CIBIL score requirements for education loans abroad?

Government banks such as SBI are generally more flexible with credit score ranges. They may approve loans even if the score is below 700, especially under schemes like the Central Sector Interest Subsidy Scheme. Private banks tend to require scores closer to the best CIBIL score range of 750+.

5. Can NBFCs offer education loans for abroad studies with low credit scores?

Yes. NBFCs such as Auxilo and InCred approve education loans for students with credit scores as low as 650. Unlike banks with stricter credit score requirements, they evaluate additional factors like course details, university reputation, and the co-applicant’s income.

6. How long does improving credit score ranges for an education loan abroad take?

Raising your credit score to meet the 700+ benchmark generally takes between 6 to 12 months. Consistent on-time bill payments, reducing credit utilisation below 30%, and correcting any errors on your credit report are key to improving your score.

7. Which parent makes the best co-applicant for an education loan approval?

Choose the parent with the stronger credit profile and stable income. This may not always be the primary income earner; sometimes, mothers or other guardians have better credit scores and financial history.

8. Can secured loans help if I have a poor credit score range?

Yes, secured loans backed by collateral like property, fixed deposits, or insurance policies improve your chances of loan approval, even if your credit score is average or below the best CIBIL score range.

")

")

{kind=link}

0 Comments