Table of Contents

Student loans can be a lifeline for pursuing higher education, but repaying them can often feel like a long, uphill climb. That’s where student loan forgiveness comes in.

This comprehensive 2025 guide will explain education loan forgiveness, how it works, who qualifies, and the available programmes.

We will also cover key differences between forgiveness and discharge, pros and cons to consider, and how to make the most of your repayment strategy, especially if you are planning to study abroad and want to keep your financial future in check.

What Is Student Loan Forgiveness?

Study loan forgiveness is a federal programme that cancels or eliminates part or all of a borrower’s federal student loan debt, relieving them from the obligation to repay that portion of their loans.

These programmes are available only for federal student loans, primarily Direct Loans, and do not apply to private student loans.

How Does Student Loan Forgiveness Work?

Student loan forgiveness works by cancelling a portion or all of your federal student loan balance when you meet certain eligibility requirements tied to your career, income, or personal situation.

Forgiveness is funded by the U.S. Department of Education, meaning federal taxpayers ultimately cover it.

Here’s how the process typically works:

1. Eligibility and Loan Types

Forgiveness programmes generally apply to federal student loans, such as:

- Direct Subsidised Loans

- Direct Unsubsidised Loans

- Direct PLUS Loans

- Private student loans are not eligible.

To qualify for some programmes, you may need to consolidate older federal loans (like FFEL or Perkins Loans) into a Direct Consolidation Loan.

2. Qualifying Criteria

Each forgiveness programme has different requirements, but common qualifying conditions include:

- Working in public service, such as government or nonprofit roles

- Making 120 on-time monthly payments under an income-driven repayment (IDR) plan

- Teaching in a low-income school

- Serving in the military

- Demonstrating total and permanent disability

3. Repayment and Certification

To stay on track:

- PSLF applicants must submit an Employment Certification Form annually or when changing employers.

- IDR plan users must recertify income and family size each year, as payments are income-based.

- You must make on-time payments—typically:

- 120 payments for PSLF

- 20–25 years of payments for IDR forgiveness

4. Application Process

Once you meet the requirements:

- Gather your loan, income, and employment records

- Contact your loan servicer to confirm eligibility

- Submit the relevant forgiveness application

- Each programme (e.g. PSLF, TPD, Teacher Forgiveness) has its own form and process.

- Processing times can take a few weeks to several months.

5. Approval and Discharge

If your application is approved:

- Your remaining loan balance is forgiven

- You are no longer required to make payments

- Forgiven debt is not taxed federally through at least 2025

Interested in student loan forgiveness options?

Explore how an abroad education loan can support your study abroad journey and how you could benefit from future loan forgiveness programmes.

Difference Between Student Loan Forgiveness And Student Loan Discharge

While both student loan forgiveness and student loan discharge lead to the cancellation of your student debt, they happen under very different circumstances.

One rewards years of service or consistent repayment, while the other offers relief due to unforeseen hardships or legal issues.

Here’s a quick comparison to help you understand how they differ and which one might apply to your situation:

| Aspect | Student Loan Forgiveness | Student Loan Discharge |

| Reason for Cancellation | Employment/ service accomplishments | Hardship, disability, death, or school issues |

| Typical Eligibility | Working in qualifying public service jobs | Disability, death, school closure, fraud, bankruptcy |

| Examples | PSLF, Teacher Loan Forgiveness | TPD Discharge, Closed School Discharge, Death Discharge |

| Application Requirement | Must certify employment and payments | Must provide documentation of hardship or event |

| Tax Implications | Usually tax-free federally (at least through 2025) | May be tax-free depending on programme |

Types Of Student Loan Forgiveness Programmes

1. Public Service Loan Forgiveness (PSLF)

Public Service Loan Forgiveness (PSLF) is a U.S. government programme that helps people working in certain public jobs get their student loans forgiven.

If you work full-time for a government agency or a non-profit organisation and make 120 monthly payments (that’s 10 years of payments), the rest of your student loan can be cancelled completely.

To qualify, you need to:

- Have federal student loans (not private)

- Be on a qualifying repayment plan (usually income-driven)

- Work for a qualified employer, like a public school, hospital, or government office

2. Teacher Loan Forgiveness (TLF)

Teacher Loan Forgiveness (TLF) is a U.S. government programme designed to help teachers reduce their student loan burden.

If you’ve worked full-time as a teacher for five consecutive years at a low-income school or educational service agency, you may be eligible to have up to $5000 or 17,500 of your federal student loans forgiven.

To qualify, you need to:

- Have federal Direct or Stafford loans

- Teach full time eligible school or educational service agency (usually listed by the government)

- Be a highly qualified teacher (meet subject-area and certification requirements)

3. Income-Driven Repayment (IDR) Forgiveness

Income-Driven Repayment (IDR) Forgiveness is a programme that cancels the remaining balance on your federal student loans if you have been making payments based on your income for an extended period, typically 20 to 25 years.

Under an IDR plan, your monthly payments are calculated based on how much you earn and your family size, not how much you owe.

You may qualify for forgiveness if you:

- Enrol in an eligible IDR plan (like PAYE, REPAYE, IBR, or ICR)

- Make consistent, on-time payments for 20 or 25 years, depending on the plan

- Have federal student loans (not private)

4. Income-Contingent Repayment (ICR)

Income-Contingent Repayment (ICR) is a federal student loan repayment plan that adjusts your monthly payments based on your income, family size, and total loan amount.

It is designed to make repaying student loans more manageable, especially for borrowers with lower incomes or those pursuing public service careers.

You may qualify for forgiveness if you:

- Make consistent monthly payments under the ICR plan for 25 years

- Have a federal Direct Loan (or consolidate eligible federal loans into a Direct Consolidation Loan)

- Are repaying a Parent PLUS Loan through a Direct Consolidation Loan enrolled in ICR

- Maintain eligibility by recertifying your income and family size annually.

5. Pay As You Earn (PAYE)

PAYE is a federal Income-Driven Repayment (IDR) plan that lowers your monthly student loan payments based on your income and family size. It’s designed to make loan repayment more affordable, especially for recent graduates with high debt-to-income ratios.

You may qualify for forgiveness if you:

- Stay on the PAYE plan and make consistent payments for 20 years

- Maintain eligible federal loans (not private or Parent PLUS)

- Recertify income and family size annually

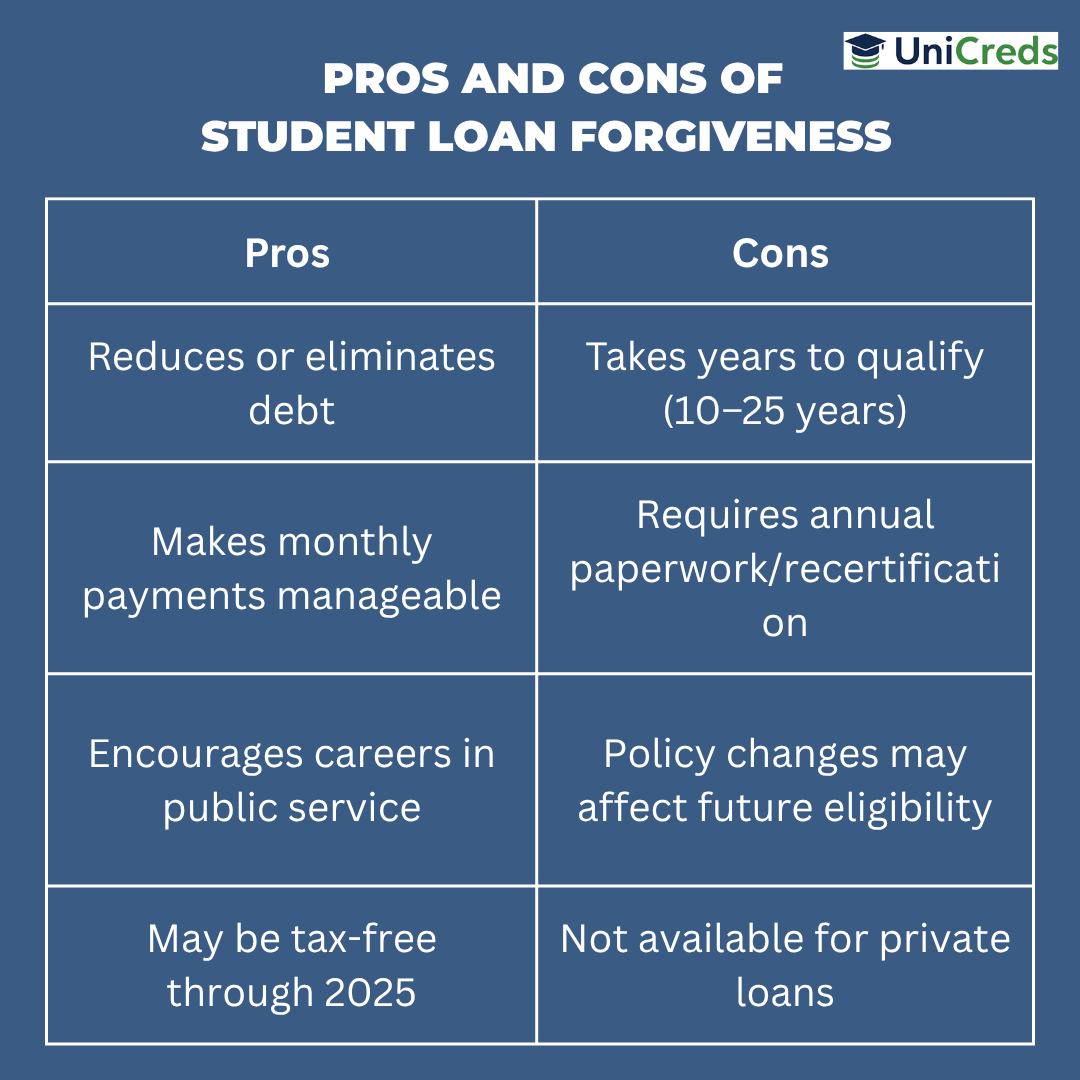

Pros And Cons Of Student Loans Being Forgiven

Student loan forgiveness can be a life-changing opportunity, but it’s not without its challenges.

While it promises reduced debt and manageable payments, it also comes with long timelines, strict requirements, and potential policy shifts.

| Pros | Cons |

| Reduces or eliminates debt | Takes years to qualify (10–25 years) |

| Makes monthly payments manageable | Requires annual paperwork/recertification |

| Encourages careers in public service | Policy changes may affect future eligibility |

| May be tax-free through 2025 | Not available for private loans |

Student loan forgiveness isn’t a one-size-fits-all solution, but for many borrowers, it can be a powerful path to long-term financial relief.

Whether you are working in public service, teaching in a high-need school, managing loans on a modest income, or navigating a life-changing disability, a programme may be designed for your situation.

Understanding your options, staying on top of paperwork, and choosing the right repayment plan are key to unlocking the benefits of forgiveness.

While it takes time and consistency, the outcome can be well worth it—less debt, lower stress, and greater freedom to plan your future.

If you plan to study abroad, making wise financial decisions from the start is just as important.

That’s where UniCreds comes in. From helping you secure the best education loan with low interest rates to guiding you on repayment options, UniCreds has your back.

FAQs

1. Are student loans eligible for forgiveness?

Yes, federal student loans may be eligible for forgiveness through programmes like PSLF, Teacher Loan Forgiveness, IDR forgiveness, and more. However, private student loans do not qualify for federal forgiveness programmes.

2. How do I know if my student loans will be forgiven?

You can check if your student loans are eligible for forgiveness by reviewing your loan type, repayment plan, and employment history on StudentAid.gov. If you meet the criteria for a programme like PSLF, IDR forgiveness, or Teacher Loan Forgiveness, your loan servicer or the PSLF Help Tool will indicate your eligibility status.

3. What happens if I can’t pay off my student loans?

If you can’t pay off your student loans, you may become delinquent or go into default, which can damage your credit and lead to wage garnishment or collection actions. To avoid this, explore options like income-driven repayment plans, deferment or forbearance, or applying for loan forgiveness or discharge based on your situation.

4. How do you cancel a student loan?

To cancel a student loan, you must apply for a federal loan forgiveness or discharge programme that fits your situation, such as Public Service Loan Forgiveness (PSLF), Total and Permanent Disability (TPD) Discharge, or Closed School Discharge. You will need to submit the required application and documentation through your loan servicer or on StudentAid.gov.

")

")

{kind=link}

0 Comments